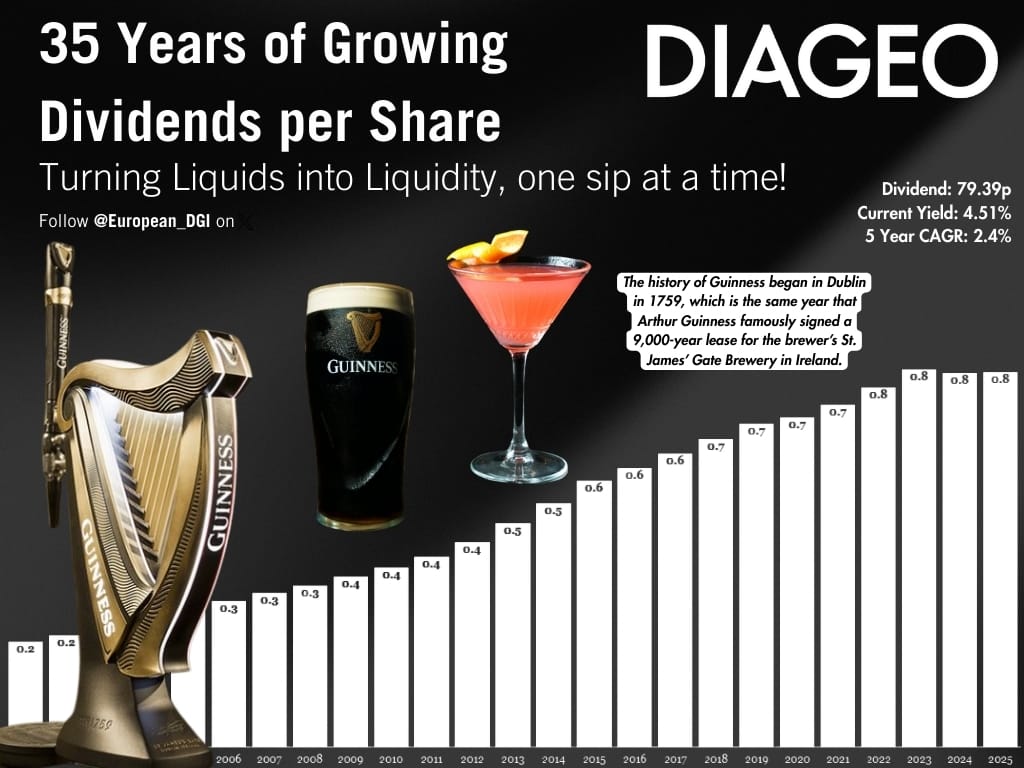

This week, we are diving deep into Diageo, a company that has been frequently discussed, as its share price has steadily declined since 2022.

Of course, it is impossible to talk about Diageo from an Irish perspective without thinking about Guinness. ( Yes, that is a home Guinness pump and a perfect pint 🙂)

The history of Guinness began in Dublin in 1759, which is the same year that Arthur Guinness famously signed a 9,000-year lease for the brewer’s St. James’ Gate Brewery in Ireland.

However, here are some fun facts about consumption: the United Kingdom is the undisputed king of Guinness drinking, topping the charts for the most pints consumed worldwide, a standing possibly helped by its proximity to Ireland.

In fact, it has been reported that one out of every 10 pints sold in London is a Guinness, and in December 2022, Guinness became Britain’s number one beer in the on-trade, with Brits drinking around 2.2 million pints every day.

This surprised me, as the storehouse is based here in Dublin (and is worth visiting), but Nigeria is up there and often surpasses Ireland for total sales.

That said, Diageo is more than just Guinness, and although it is my favourite tipple, I will not let that cloud my judgement when looking through the company, and I can promise there was no consumption of Guinness during this Article 🙂

So, get your favourite beer ready and enjoy today’s deep dive.

Yours Truly

Derek

| Note: We call this an in-depth analysis because we thoroughly examined the available information. However, we do prefer to keep our writing digestible. That’s why not every detail we found is written down, but feel free to follow up if you have any further questions. |

| Mission statement: To create the best performing, most trusted and respected consumer products companies in the world. Our Business | The Blend | Diageo |

About Diageo

Diageo Plc (DGE.L) has long been regarded as a UK aristocrat and a core holding for many investors focusing on income or dividends. The Investment case was straightforward; their customers had a tendency to drink better and not more, known as premiumisation, and the rise of the middle class, particularly in the emerging markets.

This strategy worked exceptionally well for nearly two decades, which is why Diageo’s decision to keep the dividend flat came as a surprise and raised plenty of questions.

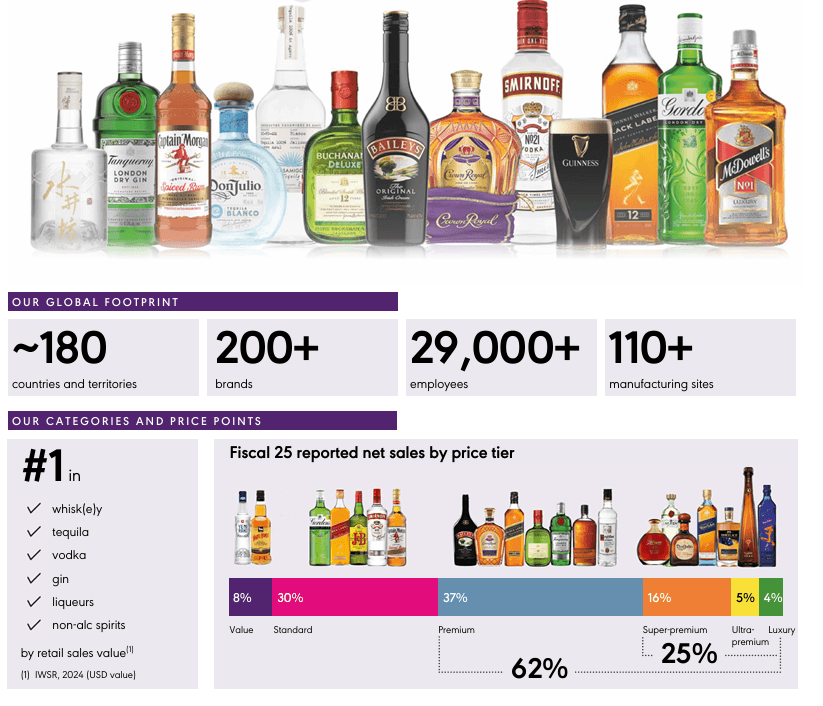

Diageo is a multinational beverage alcohol company formed in 1997 through the merger of Grand Metropolitan and Guinness plc. The combination brought together centuries of brewing heritage with deep distillation expertise, creating a portfolio that now spans more than 200 brands sold in nearly 180 countries.

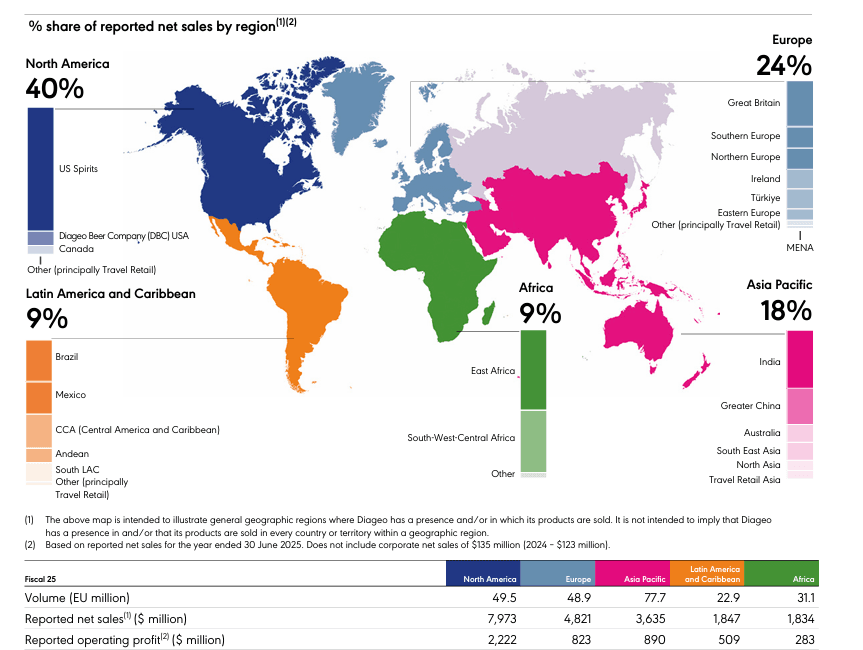

The company is headquartered in London but operates through five major geographic regions: North America, Europe, Asia-Pacific, Latin America & the Caribbean (LAC) and Africa.

There was a time when Diageo looked very different. It owned food-related businesses such as Burger King and Pillsbury, but divested them in 2000 to focus on higher-margin premium drinks and to strengthen what would eventually become the “Diageo Advantage”: Brand Power, Premiumisation, and Global Distribution.

Today, Diageo’s portfolio includes some of the most recognisable names in global beverages: Johnnie Walker, Don Julio, Smirnoff, Tanqueray, Gordon’s, Baileys, Captain Morgan, and, of course, Guinness (several of which happen to be among my personal favourites)

In my deep dive on Pernod Ricard, I mentioned how impressed I was with their ability to acquire companies while preserving the identity of the underlying brands. When I think about Diageo, I would argue they’ve taken this one step further: their brands are deeply woven into cultural relevance, national identity, and even generational drinking habits.

This is especially true for Guinness, which has an almost emotional connection to Ireland (even though England is its largest market), and Johnnie Walker, which represents aspirational success across Latin America.

Brands like these shorten the decision-making process for consumers. Familiarity and trust guide choices almost subconsciously. For example, if I walk into an airport, I will generally default to buying Guinness without much thought.

This instinctive behaviour gives Diageo significant pricing power. Consumers aren’t comparing drinks purely on taste or alcohol content—they’re buying into identity, emotion, and the experience associated with the brand.

This creates a flywheel for Diageo:

- Retailers feel compelled to stock Diageo products because they drive traffic.

- Distributors prioritise the portfolio because it sells consistently.

- Bartenders and mixologists favour Diageo brands because consumers ask for them by name.

Basically, the strength of the brand portfolio becomes a self-reinforcing loop.

But while brand strength draws consumers in, distribution ensures that these products are available wherever and whenever consumers expect them. Spirits is a heavily regulated industry with complex supply chains that vary significantly by region.

Diageo’s global distribution network, built over decades through partnerships, is one of the most sophisticated in the world.

For example, in the United States, the industry operates under a three-tier system, which often adds complexity for smaller companies. Diageo’s scale turns that complexity into an advantage.

Its portfolio is simply too valuable for distributors to ignore, allowing Diageo to negotiate favourable placement, stronger selling support, and deep marketing collaboration.

How do they make money?

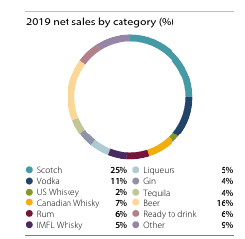

I looked at this from two different angles, one was in 2019, which was just before COVID, and the second was how that evolved to today.

In 2019, Scotch was the main driver, accounting for 25% of sales. For as long as I’ve known Diageo, they’ve been predominantly a scotch company. Beer, led by Guinness, accounted for another 16% of the portfolio, while Tequila accounted for only 4% of the business.

This type of product mix was stable, predictable, and deep in brand equity, linked to the cultural heritage I mentioned earlier. But drinking habits change, and maybe COVID accelerated this, but consumer preferences worldwide are shifting rapidly toward more premium experiences.

Fast forward to today, and Tequila now accounts for 13% of the business. Scotch’s share of the portfolio declined slightly to about 22% as the category faced weaker demand in China and slower momentum in travel retail.

Beer, however, strengthened to around 18% of net sales, driven by a remarkable resurgence of Guinness. (You’re welcome, shareholders 🙂)

This global shift in preferences almost coincided with its premium and super-premium spirits strategy, where premium and above now accounts for more than 65% of sales.

Even more impressive, the super-premium-plus category, so not just better brands, but true luxury brands, has been growing more than 50% faster than the rest of the industry.

What I like about this strategy is that premium tiers don’t need to grow at a high rate to deliver meaningful profit increases. That makes them a very important part of Diageo’s long-term plan. As a consumer, though, I have a different thought!

The product mix is only half the story, given Diageo’s global diversity.

North America, in particular the U.S., is the world’s most premiumised spirits market, with high consumer willingness to spend on brands perceived as authentic or high-quality.

What this tells me is that when North America performs strongly, Diageo performs well, but when North America weakens, the entire business feels the impact.

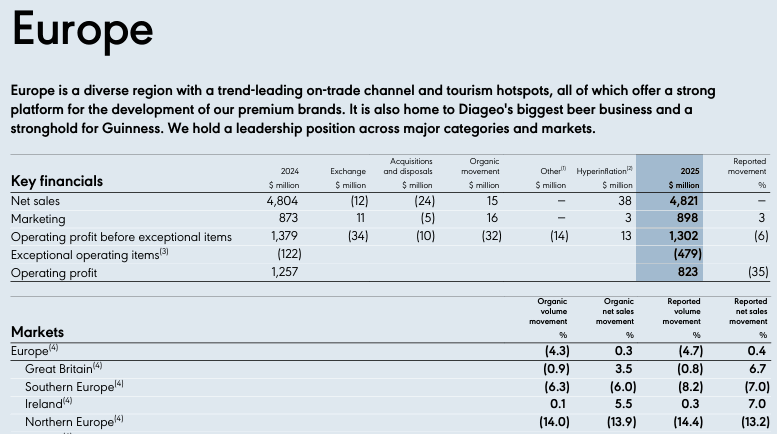

Europe is a little different, even though it is the second-largest market in terms of sales. We won’t see the same growth as in the US, but it is steady, led by Ireland and the UK, thanks to Guinness, including Guinness 00.

Asia Pacific is more of a mixed bag today. China is soft, and that naturally hits Scotch the hardest. But India is making up for it. The combination of a rising middle class, increasing disposable income and a strong appetite for premium spirits makes India one of Diageo’s most attractive long-term markets.

Growth Catalysts?

2025 has been a tough year for Diageo, and the share price reflects that. When a company underperforms the wider market by such a margin, it becomes harder to separate genuine issues from the noise driven by shifting sentiment.

One of the louder narratives is that younger adults are drinking less and prioritising a healthier lifestyle. There’s truth to that and we have mentioned this on the podcast many times over the last number of years, but that only applies in certain parts of the world.

From a Western, first-world perspective, it looks like alcohol consumption is falling with the Gen Z generation. But Diageo’s long-term growth doesn’t hinge on Europe or the U.S.

It hinges on the rising global middle class, where consumption habits look very different. Over the next decade, it is estimated that roughly 600 million people will reach legal drinking age.

That alone is a strong growth driver. And as these younger adults enter the market, particularly in developing economies, the opportunity is not just about drinking more, but drinking better.

At the same time, consumers everywhere have been under pressure. We’ve seen weakness across multiple sectors, even if the performance of the “Magnificent 7” has masked just how fragile many economies have been over the last few years. Inflation has hit the consumer hard.

My views about behaviour shift to alcohol obviously stem from Ireland, which is a relatively small country. In Ireland, younger people are not following the patterns of previous generations.

For example, when I was a young adult playing on a sports team, it was common to go out for a beer or two after a game. It would never be spirits, just beer. So, for me, the catalyst here is that more consumers are entering through premium products.

And there’s no better example than India.

India combines everything Diageo wants: a huge, young population (median age under thirty), rising incomes, rapid urbanisation, and a drinking culture that is gradually shifting from value spirits to premium offerings.

Western-style drinks and cocktail culture are growing fast, and as affordability improves, premium spirits are becoming a natural product for the expanding middle class.

It purely boils down to management execution here.

But if we stick to the theme that consumers are looking for healthier alternatives that still deliver the brand experience, non-alcoholic options have good growth potential.

I have and will probably never try it 🙂 But Guinness 0.0 has quickly become the leading non-alcoholic beer in Great Britain, proving that when you take an iconic brand and authentically translate it into a zero-alcohol format, consumers will respond.

What is interesting about these drinks is that they have minimal excise tax, since they’re not alcoholic. Still, they’re often priced higher than the alcoholic version, which can only help with margin expansion.

The exit of CEO Debra Crew during a transformation was not ideal, and given how fragile the market is, fragile management or leadership instability was the last thing the company needed.

That’s why the announcement of Sir Dave Lewis, better known as “Drastic Dave”, as the new CEO triggered such an immediate shift in sentiment. His track record at Tesco and Unilever before that is well known.

He steps into messy situations, simplifies operations, cuts unnecessary complexity, and rebuilds performance with discipline and speed. Knowing how he handled and turned around Tesco, I believe he is an excellent choice for Diageo, and I’ll be interested to see how his bonuses are laid out in the next annual report.

Diageo drafts in ‘Drastic Dave’ to revive spirits giant

Business Performance

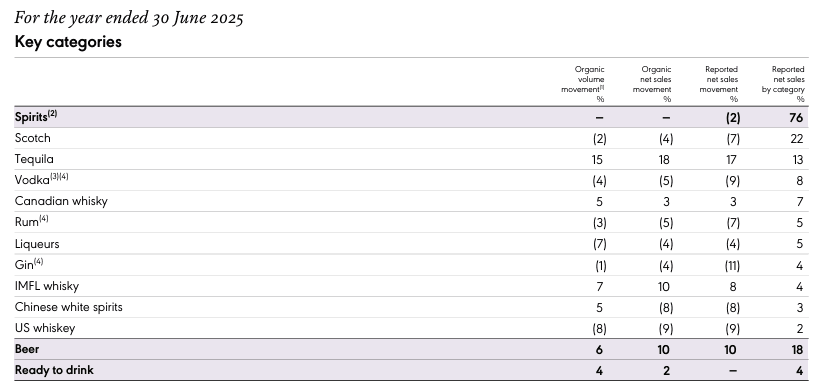

Diageo tracks its top-line performance through organic net sales growth, which is essentially revenue growth stripped of currency swings, acquisitions, and disposals. This gives us a clean view of how the brands actually performed in the market over the last decade.

For the above chart, revenue is estimated in USD for years before 2023, when it was reported in GBP. However, ignoring the actual revenue numbers, I extracted the sales growth and the impact of volume growth in the table below.

| FY | Net Sales | Sales Growth | Key Growth Drivers |

| 2016 | £10,485 m | 2.80% | 1.3% volume growth |

| 2017 | £12,050 m | 4.30% | 1.1% volume growth. |

| 2018 | £12,163 m | 5.00% | 2.5% volume growth. |

| 2019 | £12,867 m | 6.10% | 2.3% volume growth. |

| 2020 | £11,752 m | (8.4%) | 11.2% volume reduction. |

| 2021 | £12,733 m | 16.00% | 11.2% volume growth |

| 2022 | £15,452 m | 21.40% | 10.3% volume growth |

| 2023 | $20,555 m | 6.50% | 0.8% volume decline. |

| 2024 | $20,269 m | (1%) | 4% volume decline |

| 2025 | $20,245 m | 2% | 0.9% volume growth |

From 2016 to 2019, net sales grew by 3% to 6% each year, driven by a mix of premiumisation and volume gains of 1% to 2%. These were steady and predictable, and precisely what you would expect from a consumer staple.

Lockdown hit relatively hard, as we saw an 8.4% organic decline, but the recovery was really impressive right up to 2022. It’s been a couple of weak years in 2023 and 2024, but given inflation and a weak consumer, particularly in the US, the volume decline hasn’t been as bad as I first thought.

And we are back to volume growth in 2025.

The fear of declining volume may be overstated in my mind. But when we look at net sales growth, which includes volume and price-mix, we can really see the effects of premiumization.

Diageo has steadily expanded margins over the past 10 years despite pressures such as overhead costs and inflation. Premiumisation and ongoing operational gains did most of the work, quietly pushing profitability higher as consumers continued to “drink better, not more”.

When consumers trade up, whether to Johnnie Walker Black, Don Julio, Guinness 0.0, Casamigos or luxury scotch, the margin profile moves with them. And Diageo’s multi-year efficiency programmes consistently reduced costs, streamlined manufacturing, improved logistics and helped to offset inflation when needed.

The fact that Diageo could often expand margins during some challenging environments speaks to the strength of the premium spirits model. The bottom line looks just as consistent and was only broken by two major shocks, COVID in 2020 and a large impairment in 2025.

| FY | Net Income | EPS |

| 2016 | £2,362 | 89.4p |

| 2017 | £2,772 | 106.0p |

| 2018 | £3,144 | 121.7p |

| 2019 | £3,337 | 130.7p |

| 2020 | £1,454 | 60.1p |

| 2021 | £2,799 | 113.8p |

| 2022 | £3,338 | 140.2p |

| 2023 | $4,479 | 164.9p / $1.79 |

| 2024 | $4,166 | 173.2c |

| 2025 | $2,538 | 105.9c |

The impairment charges in 2025 were the single biggest reason Diageo’s reported profit fell so sharply. In total, Diageo wrote down over $1.3 billion, with $910 million of that tied to assets and brands that no longer justify their carrying value.

The largest hit came from Distill Ventures, where Diageo effectively admitted that the innovation pipeline it had been funding for years wasn’t delivering the scale or returns it had hoped for.

Aviation American Gin and several newer US whiskey assets were also written down due to a softer category environment. Even Bell’s, once a core mainstream whisky, was impaired as Diageo continues to shift its focus firmly toward premium and above.

Diageo is clearly drawing a line under the more experimental, venture-style acquisitions of the past decade and driving more towards tequila, scotch, Guinness and non-alcoholic offerings. In that sense, cleaning up the balance sheet was needed.

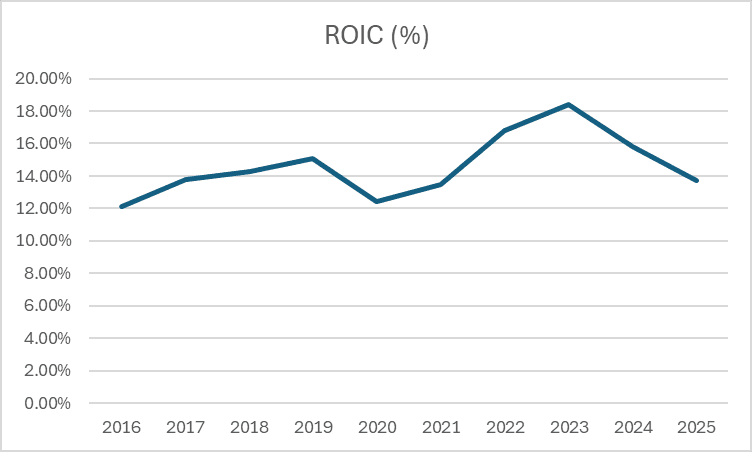

Diageo’s return on invested capital is one of the clearest indicators of how effectively the company is turning its asset base into real profit. After a couple of good years after COVID, ROIC has been declining thanks to lower income from Moët Hennessy, currency headwinds, and a growing invested-capital base, which weigh on the calculation.

The expansion of invested capital is partly due to Diageo’s aggressive acquisition policy, such as the 2019 acquisition of Copper Dog Whiskey and the 2023 acquisition of Don Papa Rum.

When invested capital grows faster than operating profit, ROIC falls even if the business is healthy. This is what happened to Diageo in 2024 and 2025 and not necessarily based on if it can support further growth.

Business Performance Conclusion

Diageo’s performance over the past decade shows exactly why it was a staple in many portfolios. Its entire model is built around a premiumisation strategy, and that theme runs consistently through its numbers.

Even when the industry hit turbulence, such as the pandemic in 2020, inflation in 2023, and regional softness in the US in 2024, the “drink better, not more” philosophy has pretty much held up.

Higher-margin brands like Johnnie Walker, Don Julio and the luxury Scotch portfolio continued to drive the business forward,and in several of the tougher years, strong pricing more than offset weaker volumes. That is the hallmark of a strong company with pricing power.

Overall, the company has shown that its business model works. Despite the significant impairment, which is a warning for future acquisitions, it doesn’t change the portfolio’s underlying strength or the company’s ability to turn global brands into reliable returns on capital.

The return to volume growth in 2025 reinforces my belief that the core demand picture remains healthy, and it suggests that business is emerging from its transition period.

Dividend Safety

All of our analysis focuses on finding companies we believe have a safe dividend profile while acquiring them at an attractive price. As a reminder for our new members, check out our wiki on how we approach dividend safety. To break it down in its simplest form, it is centred around five key questions.

- Does the company grow

- What are the company’s growth catalysts

- Do they have a healthy Balance Sheet

- Can they afford the dividend now and into the future

- Has the management shown commitment to the dividend?

The first two questions are answered in the first part. The company has been growing over the last decade. There was a bump in the road after 2022, attributed to a change in drinking culture, but it was mainly due to inflation and a weaker consumer. Management has really been executing its premiumization strategy quite well, which is also improving the quality of its earnings. Its cayalts remain the ever-growing middle class, especially in areas like India, where millions of people will turn 18 and enter the legal drinking age. And for those who may be more health-conscious, there is the 00 brands.

Now we need to answer the remaining three questions.

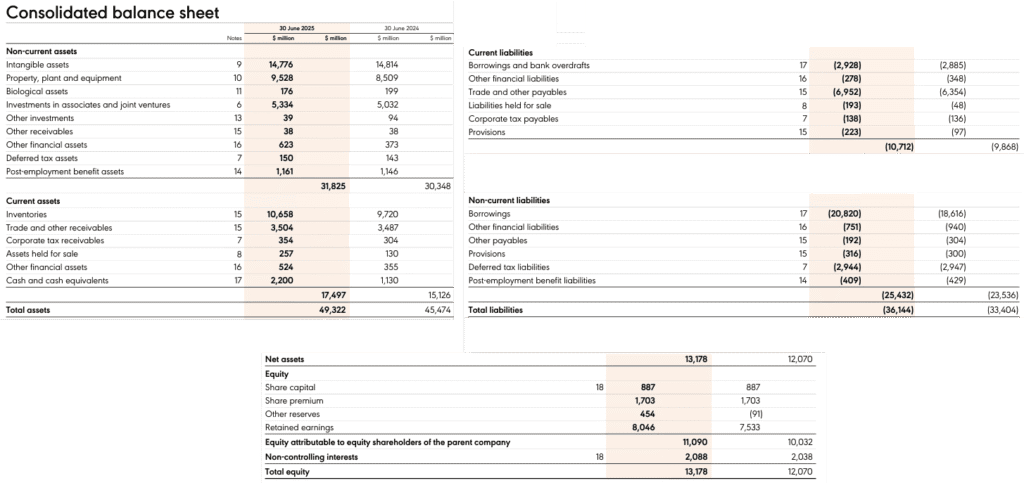

Do they have a Healthy Balance Sheet?

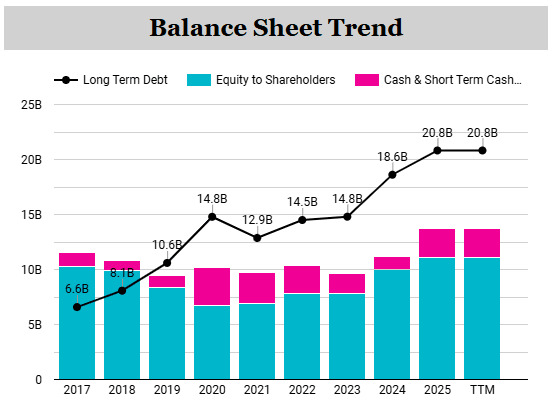

The company targets a net debt-to-EBITDA range of 2.5–3.0x, which it considers appropriate to maintain an A-band credit rating. Diageo sits comfortably within this range most of the time, apart from the COVID year.

| FY | Net Debt | EBITDA | Net Debt to EBITDA |

| 2017 | £8,664m | £4,271m | 2 |

| 2018 | £9,963m | £4,496m | 2.2 |

| 2019 | £12,123m | £4,802m | 2.5 |

| 2020 | £13,995m | £4,270m | 3.3 |

| 2021 | £12,683m | £4,527m | 2.8 |

| 2022 | £14,539m | £5,703m | 2.5 |

| 2023 | $20,053m | $7,353m | 2.7 |

| 2024 | $21,446m | $7,037m | 3 |

| 2025 | $22,263m | $6,645m | 3.4 |

In 2025, its leverage spiked to 3.4x on the back of the significant impairments that we discussed earlier, and adverse FX movements on non-USD debt. As the company changed its reporting to USD the weakening of Sterling and Euro debt against the US Dollar pushed the ratio up to 3 in 2024.

Management expects to be back within the 2.5 to 3x range “no later” than 2028, and I will give management the benefit of the doubt here based on its history of deleveraging after periods of volatility.

The company holds more than $2.7 billion in cash and short-term financial assets and backs this up with $3.5 billion in committed credit facilities. Even in 2025, a year where impairments hit profits, the business still generated $2.7 billion in free cash flow, comfortably covering its near-term refinancing requirements. Its short-term debt of around $2.9 billion is almost entirely covered by cash on hand. More importantly, Interest coverage stands at 8.6x, which is more than enough for a consumer staple.

Working capital has grown as the company has scaled, particularly in inventory, which exceeded $10.6 billion in 2025. But this is the nature of a spirits business; for example, Scotch and tequila age for years before sale, and accounting rules classify all maturing stock as “current,” even though the cash comes back much later.

Goodwill in relation to its assets is around 6.3% in 2025, for context, it was around 9.47% in 2016. But goodwill and Intangibles have ballooned from £12.5 billion to just over £30 billion. This now makes up roughly two-thirds of the total asset base, compared with about 40% a decade ago.

| FY | Goodwill | Intangibles | Other Intangibles | Total G/I | Assets | GW/ A |

| 2016 | £2,699 | £8,079 | £1,592 | £12,370 | £28,491 | 43% |

| 2018 | £2,678 | £8,330 | £1,564 | £12,572 | £29,715 | 42% |

| 2019 | £2,682 | £8,274 | £1,601 | £12,557 | £31,296 | 40% |

| 2024 | £10,486 | £17,739 | £1,800 | £30,025 | £45,300 | 66% |

| 2025 | £11,357 | £17,739 | £1,800 | £30,896 | £46,804 | 66% |

Some of this can be put down to the nature of the spirits industry, where brands, trademarks and maturing inventory can carry far more value than factories or machinery.

But the real step-change since 2020 is the result of a decade of premium-priced acquisitions layered on an already brand-heavy balance sheet. The impairments this year acknowledged that not all of these deals were delivering the returns initially expected. It shows the real danger of an aggressive acquisition strategy, especially in a sector where consumers’ tastes can change.

Diageo’s balance sheet is not as strong as I would like, but I would not be overly concerned about it. Leverage is slightly above management’s specified target range, and goodwill/intangibles make up most of the balance sheet. Still, cash flow is solid, liquidity is strong, and interest coverage indicates they can easily service their debts.

I guess after a decade of investment, it’s a bit of a transition phase for Diageo on the back of heavy impairments, and we should see the balance sheet strengthen as profits improve.

Can they afford the dividend?

In the 2025 Annual report, management quotes the following: “The decision in respect of the dividend is made with reference to the dividend policy for the respective period that includes current performance trends, including sales, profit after tax and cash generation. Diageo aims for dividend cover (the ratio of basic earnings per share before exceptional items to dividend per share) within the range of 1.8-2.2 times.”

Given that they mention a specific dividend cover, it makes sense to track their history using this metric.

| FY | DPS | EPS | Dividend Cover | EPS Payout Ratio | FCF | Dividend | FCF Payout Ratio (%) |

| 2016 | 59.2 | 89.4 | 1.51 | 66.22% | 2097 | 1443 | 68.81% |

| 2017 | 62.2 | 108.5 | 1.74 | 57.33% | 2663 | 1515 | 56.89% |

| 2018 | 65.3 | 118.6 | 1.82 | 55.06% | 2523 | 1581 | 62.66% |

| 2019 | 68.57 | 130.8 | 1.91 | 52.42% | 2608 | 1623 | 62.23% |

| 2020 | 69.88 | 109.4 | 1.57 | 63.88% | 1634 | 1646 | 100.73% |

| 2021 | 72.55 | 117.5 | 1.62 | 61.74% | 3037 | 1646 | 54.20% |

| 2022 | 76.18 | 151.9 | 1.99 | 50.15% | 2783 | 1718 | 61.73% |

| 2023 | 80 | 163.5 | 2.04 | 48.93% | 1830 | 1762 | 96.28% |

| 2024 | 103.48 | 179.6 | 1.74 | 57.62% | 2748 | 2243 | 81.62% |

| 2025 | 107.82 | 164.2 | 1.52 | 65.66% | 2700 | 2298 | 85.11% |

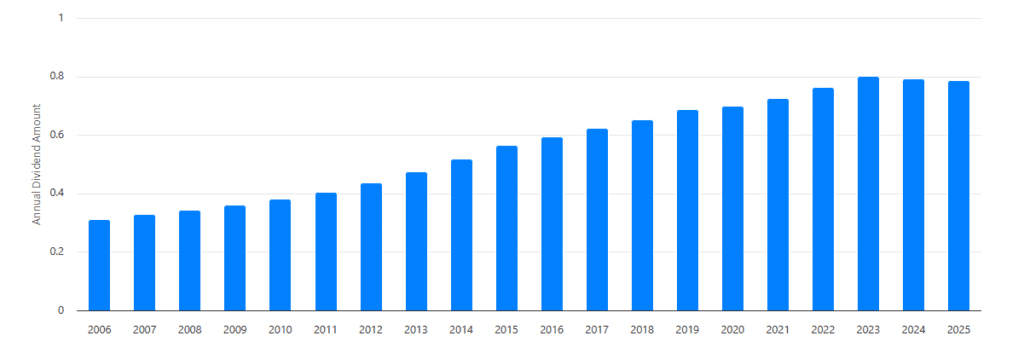

The dividend per share has grown at a 6.89% CAGR since 2016 (note I know they changed to USD in 2024, but I ignored it for the time being to keep the calculations easy). Earnings during the same period have grown at a 6.99% CAGR.

Growing dividends at the same rate as earnings growth is sustainable in the long term, so I like to see this, but the dividend cover is below management’s target. A Dividend of over 1.5 translates to a payout ratio of 65.66% which is not an immediate concern, but does not give much wiggle room to grow if we continue to see pressure on profits.

A dividend cover of 1.5 is not an immediate concern, but it’s worth monitoring, and I would like to see how management would act in this scenario. Do they stick to their target and potentially cut the dividend to meet it, or do they lower the target? They have never really had a prolonged period of dividend cover below their target.

I have no crystal ball, unfortunately, but we can look at management’s commitment to the dividend, and they have raised its dividend since 2001. However, they have kept it flat in 2025 from 2024. It might look like a small dividend cut in 2024 but they switched from GBP to USD as dividend payments, hence the slight decline in 2024 and 2025 due to currency impact.

Looking at the numbers, keeping the dividend flat is not surprising given the deterioration in dividend cover below 1.8.

What is surprising is that we have a company with a “progressive dividend “ that has increased its dividend every year since 2001, through recessions and COVID, but has suddenly kept it flat.

Pay-out ratios from earnings are one thing, but dividends are paid in cold, hard cash, which is why I prefer to look at free cash flow irrespective of the company’s dividend policy.

While earnings payout ratios are generally in the safe range, FCF has been on the high end in the last three years. This also coincides with the debt rising during the same period. For a company that acquires brands as part of its strategy and requires innovation to stay ahead of competitors, 80%+ FCF payout ratios are too high.

Diageo is a consistent cash generator, but Free cash flow has grown at 2.85% since 2016, compared with 5.31% in dollar terms for total dividends paid. The demands on cash pile are rising with maturing stock, capex for capacity expansion, higher interest costs, and a balance sheet temporarily operating outside the leverage target range.

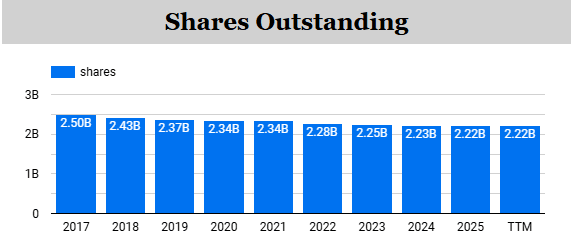

The company’s buyback program has helped in the past (even at silly valuations), contributing to some of the EPS growth I mentioned earlier, but with cash tight, the company has paused the buybacks, which might slow EPS growth and, by extension, dividend growth.

Dividend Safety Conclusion?

Diageo currently trades with a dividend yield of 4.58%, which is typically higher than its historical level. In the last dividend stock card, EDGI wrote:

“We believe the dividend remains safe for now, as management is effectively driving cost savings to support free cash flow. That said, watch execution closely, a drop below £2.5 billion in annual free cash flow would undoubtedly put the dividend at risk.”

This still remains true, but I would add to this. The £2.5 billion level to keep the dividend safe is provided, on the condition that the dividend remains flat. With dividend growth incorporated, we need to see whether the company increases its bottom line back to the levels we saw in 2022 and 2023.

I have to be honest and went back and forth on whether I think the dividend is safe, but ultimately I agreed that EDGI’s dividend is safe, though with a limited margin. It’s the dividend growth part I am not as confident in.

I stuck with the score of 62/100 on the basis that we have seen volume growth in 2025, and we are near the bottom of the cycle, and management has an excellent track record in delivering even during challenging times.

Valuation

From a valuation perspective, Diageo looks very different today than it did during its “quality at any price” phase. For most of the past decade, the market was happy to pay around 22× earnings, which implied an earnings yield of roughly 4.5%.

At that time, the growth outlook was steady, premiumisation was powering margins, and debt levels were more conservative, so the premium multiple made sense.

Today, the picture is more subdued. The shares trade at 1742p, and with EPS of 164 cents (roughly 126p), the stock now sits close to a 14× P/E. That equates to an earnings yield of about 7.1%, suggesting the market no longer views Diageo as a flawless compounder. It’s more like a stable consumer staples business working through a downcycle. The price-to-free-cash-flow multiple tells a similar story.

Is 14× cheap? Not absolutely, but it’s certainly much more reasonable than the 22–25× range Diageo traded at in 2021. A 14× multiple implies that the business only needs to grow EPS around 3% per year to deliver a 10% total return. If you prefer the stricter “earnings + dividends” method, you’d be looking for roughly 5.5% earnings growth alongside a 4%–4.5% dividend yield.

If history is a guide, Diageo has achieved that many times in its past.

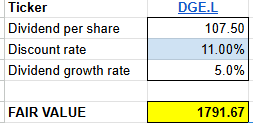

For our Dividend Discount Model, I have used the following assumptions.

- 107.5 c dps

- 11% required return

- 5% dividend growth rate

Based on what we discussed earlier, the 5% dividend growth depends on the company getting back on track with bottom-line growth. That said, it is optimistic given the company’s leverage and growth over the last couple of years.

The only positive is that the company has a good track record of navigating cycles, and it returned to some small-volume growth in 2025. If this is the bottom of the cycle, then this 5% is easily achievable.

If I am wrong and the alcohol business is in a decline similar to what we see with cigarette stocks, then this 5% could be overstated, and the dividend would be in danger, negating the DDM.

I am leaning towards a cyclical outlook, so I am optimistic about 5% dividend growth, giving a fair value of £17.91, which is pretty much in line with the share price today.

For our DCF model, I have used the following assumptions:

- 2.7 billion of free cash flow

- 4% growth for the first 5 years and 3% for the next 5. Again with the narrative of being close to the bottom of a cycle.

- 11% discount rate, which is my required return

- A 15-terminal multiple.

Plugging all this in yields a fair value of £17.55, which is again pretty close to where the company is trading today.

Considering all of this, I think it is fair to say that the fair value price for me sits between £17 and £18. It’s not a bargain at this price, but if management execution is good, it is in an interesting zone.

Top Risks

Diageo is committed to a progressive dividend, and management highlights dividend cover of 1.8–2.2x as the cornerstone of that policy. But dividend cover is only as strong as the earnings and cash flow underpinning it. Here are some risks that could compromise Diageo’s ability to maintain or grow the dividend.

Leverage and Capital Allocation: The spirits industry is capital-intensive, with high working capital requirements, and Diageo has relied heavily on debt over the past decade.

Diageo’s self-imposed leverage target of 2.5–3.0× net debt to EBITDA is designed to keep the balance sheet in A-band credit territory, ensuring access to low-cost funding.

The problem is that we are above this limit, which limits capital allocation. Diageo was forced to prioritise balance sheet stability over capital returns, with share buybacks paused until conditions normalised. If we continue to see soft earnings, this will limit the scope for growth, and dividends will become more sensitive to FCF fluctuations.

📣 Likelihood of happening in the next 5 years: medium, impact: high

Failure to Execute the Growth Strategy: Diageo must simply keep growing its earnings. The entire dividend policy relies on consistent operating profit growth, supported by premiumisation, pricing and innovation.

Acquisitions have historically played a role in its growth story, but the recent impairments are a reminder that not every deal will deliver the returns Diageo hoped for.

That makes execution more important than ever, and incoming CEO Sir Dave Lewis, known as a turnaround king, will have all eyes on how he executes it and takes advantage of the catalyst we spoke about earlier.

📣 Likelihood of happening in the next 5 years: medium, impact: high

The US and India Markets: Another real risk is that Diageo simply fails to capitalise on the markets that are actually growing. The U.S., which has long been the growth driver for Diageo, is cooling a bit as young adults drink less.

But not all markets are equal, and, as discussed, over 600 million new adults will reach drinking age over the next few years. India is an obvious growth market, but just because the market is growing does not mean consumers will choose Diageo’s products.

It is a balancing act for the time being, where they need to keep market share and stay up to date on drinking trends in mature regions, while at the same time putting their products front and centre in growing markets.

📣 Likelihood of happening in the next 5 years: low, impact: medium

Final Thoughts

First and foremost, I’m a Diageo customer. If I’m out for “one” (and any Irish person knows that usually means) it’s Guinness in my hand. But being a customer and being an investor are two very different things, and I didn’t want that bias creeping into this analysis.

I’ll be honest: I went back and forth throughout this deep dive. When I look at the business itself, I see a lot to like. The narrative around young people abandoning alcohol feels overstated, at least globally. Yes, volumes have come down from the 2022 highs, but not to the extent I expected.

And Diageo’s strategy of “better, not more” is clearly working. Younger consumers are premiumising faster with cocktails, tequila, and higher-quality spirits and they’re drinking in more varied settings such as concerts, barbecues, sports events, and festivals.

Add to this the growing global middle class, particularly in markets like India, and you can see why the long-term demand still looks attractive.

But then there’s the other side of the story: the numbers. The balance sheet has unquestionably weakened. Leverage is up, buybacks are paused, and dividend growth has stalled. For a dividend growth investor, that makes me uncomfortable. A lot now hinges on management’s execution.

This is where Sir Dave Lewis enters the fray. His track record speaks for itself, and he’s widely regarded as someone who can simplify, refocus and deliver. The question is whether Diageo is a turnaround story or whether it’s just working through the low point of a cycle.

The small but important return to volume growth in 2025 nudges me toward the cyclical explanation, and if that’s right, the investment case starts to look interesting.

Which brings me to valuation. Buying Diageo at a 14× P/E and a 4.5% dividend yield could prove to be an excellent entry point if the company restores earnings momentum and strengthens the balance sheet.

I can easily see the market re-rating the stock back toward the high-teens multiples. But we need to be realistic and remember that dividends will follow earnings. With limited free cash flow left after capex and debt management, Diageo can’t rely on buybacks to prop up EPS anymore. Real growth is going to have to do the heavy lifting.

Taking everything into account, I’m tempted to take a position, not because the story is perfect, but because the risk/reward is starting to tilt in my favour, and I have growing confidence in the incoming CEO and the strength of the brands.

This won’t be a buy-and-forget holding. It will be a buy and will be monitored closely. And while I continue thinking it over, I’ll do my part for shareholders the Irish way: by contributing to Guinness volumes whenever I’m out for that “one.”

Yours Truly,

Derek

Disclosure of ownership at time of writing:

- European Dividend Growth Investor owns no shares in Diageo.

- Derek owns no shares in Diageo at the time of writing.